Why Isn’t Micro Four Thirds the Perfect Format?

Micro Four Thirds had a lot going for it when it launched as it promised low cost, smaller lenses, and good image quality. So why didn’t it become the go-to format?

The new mirrorless era was ushered in with the release of the Panasonic Lumix G1 in November 2008; the future was here for all to see and see they did. As an increasingly frenzied buying public hoovered up more and more cameras, so manufacturers fell over themselves to release new systems. The intention was to give budding new photographers a low-cost taster, then hook them in to buying lenses, accessories, and more expensive cameras. So why wasn’t the upstart Micro Four Thirds system the natural successor to the photographic crown?

Micro Four Thirds (MFT) has had a relatively long and iterative evolution since the birth of its spiritual father — the E-1 — back in 2003. In fact, you could probably argue that the original OM-1 was the spiritual grandfather, as that truly iconic system ushered in an era of contemporary looks married to groundbreaking design that significantly reduced size and weight. The camera proved revolutionary, catapulting Olympus into the “big five” of Japanese camera brands.

It’s ironic then, that the OM was the cause of Olympus’ digital SLR demise and subsequent rebirth in the form of the E-1. The OM-707 was the first — and last — attempt at an autofocus OM which was not only a poor effort, but probably the worst of the autofocus systems released by manufacturers in the 1980s. It ultimately changed Olympus’s strategic direction, and it instead focused on the profitable consumer bridge camera market. OM never transitioned to digital and, by the early 2000s, it was clear that an SLR was needed to fill out its range.

Olympus was not afraid to innovate and developed the E-1 from scratch to meet the perceived needs of the digital camera market. In the same way, the OM shrunk the SLR to more svelte proportions, so the E-1 brought new meaning to a portable DSLR. While Nikon and Canon were constrained by existing film cameras and lenses — meaning each opted for APS-C (and APS-H) or full-frame — Olympus had a blank canvas and, with Kodak, established the Four Thirds format, notably growing the consortium to include Panasonic and Leica.

Sensors were relatively expensive components in the early 2000s, so the 17.3mm by 13mm design offered some significant benefits. It was cheaper and, because it was smaller, the camera and lenses were also smaller and commensurately cheaper. The 2.0x crop-factor brought advantages of reach and depth-of-field and the sensor also brought along with the potential for faster readout times. The E-1 was built from the ground up for the pro news and sports segment and came with a competitive 5-megapixel Kodak sensor, dust/weather sealing, and the first sensor dust removal system (Supersonic Wave Filter), however the frame rate and AF didn’t match Canon and Nikon’s offerings.

Olympus made good with the E-3 in 2007 through significant technical improvements including fast AF and in-body image stabilization (IBIS), however the horse had already bolted by this point (even with the release of the E-5 in 2010). What’s interesting about this product timeline is that MFT arrived in 2008, Olympus’ first model was the diminutive Pen E-P1 in 2009, but it wasn’t until the release of the OM-D E-M5 in 20212 that a genuine top-line MFT model arrived.

MILCing It for All It’s Worth

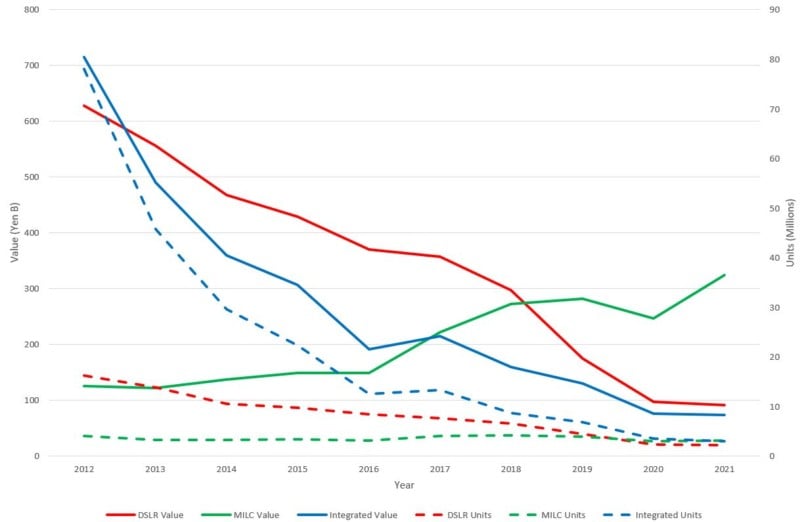

The MILC (mirrorless interchangeable lens camera) conundrum is perhaps best summarized in the chart below which shows CIPA camera shipments (units and value) by product type; in three short years, MILCs were important enough to have their own reporting, however the size of this pales when compared to integrated cameras and DSLRs. In fact, both these groups were each six times bigger!

By 2013, DSLRs became the most valuable group but were overtaken by MILCs in 2019. In fact, what’s noticeable about MILCs is that they are the only category that is growing. The BCN Awards, which track Japanese sales, show that — from 2010 — Olympus, Sony, and Panasonic took equal shares of what was a very small pie, with Canon only entering the top three in 2015. By 2021, Olympus’s (now OM Digital Solutions) share had plummeted to just over 10%.

So the question remains: where did it go wrong for Olympus and why isn’t MFT — the original mirrorless format — the format of choice?

Part of the answer lies in the original E-1. While Olympus didn’t have the baggage of an existing film system to hold it back, the inertia that photographers have from switching systems, coupled with the sluggish AF and slow frame rate (it hit three frames per second, whereas the Nikon D2Hs was capable of eight frames per second), meant it just wasn’t good enough. While the E-3 and E-5 solved these problems, the arrival of Canon’s 1-DS and 5D, followed by Nikon’s D3, D800, and D300 proved to be too much to compete with.

But it didn’t stop there. The DSLR juggernaut had gained momentum, becoming the most valuable segment by 2013. The development of the E-3 and E-5 suggests Olympus wasn’t convinced by the technical specifications of the new MFT format; the fact that Panasonic was first out of the gate and that Olympus’ model was the competent but far from inspiring Pen E-P1 shows it was testing the waters.

It would take until 2012 and the OM-D E-M5 for Olympus’s first serious camera to arrive, although it was a blinder! However, by this point, every other manufacturer was already in mirrorless full swing with the following new mounts arriving: Sony (2010, APS-C), Samsung NX (2010, APS-C), Nikon CX (2011, CX), Pentax Q and K (2011, 1/2.3-inch and APS-C), Canon EOS-M (2012, APS-C), Fujifilm X (2012, APS-C), and Leica L (2014, FF). The full-frame Sony Alpha 7 then arrived in 2013.

This veritable cornucopia of mounts shows that — at least early on — no one thought of putting a large sensor in a mirrorless camera, as these were models to supplement a DSLR. Even with APS-C the most popular choice, Fujifilm remained the only vendor who genuinely believed this could replace full-frame.

However, it was actually two unrelated events that caused Olympus’ promising start to stutter. The first of these was out of its control: the smartphone.

For a time, consumers appeared to have limitless resources to spend on cameras, peaking at 120 million units in 2010. But the rise of the smartphone put a camera in (nearly) everyone’s pocket and camera sales fell off a cliff, at a time when manufacturers were funding the expansion of new mirrorless systems.

The second was entirely of its own making: the infamous accounting scandal. With over $1.5 billion of investment losses, kickbacks, and bribes identified, it was hit with somewhere in the neighborhood of $650 million in fines in the United States and three-quarters of the company’s value was wiped out.

MILC Usurps the DSLR Crown

The replacement of DSLRs by mirrorless was never a foregone conclusion, however, the elegance of the design gives three significant technical advantages. First removing the mirror box/pentaprism makes manufacturing simpler and cheaper. Secondly, this also makes the cameras smaller and lighter. Finally, the mount can be closer to the sensor which opens up opportunities for other mount support and more efficient and esoteric designs.

This is, of course, as true for MFT as it is for full-frame models. The problem with smaller sensors has always been one of noise, although this issue has reduced somewhat as sensor design improved. Olympus would argue that MFT gives the right balance of size/weight, reach, depth-of-field, and sensor speed, making it particularly adept for news/sports, street, and home use. It’s the same argument that Fujifilm uses for the X-series, however it is able to balance this assertion with the availability of its medium format GFX.

The success of full-frame has perhaps less to do with principle benefits and more to do with marketing and the manufacturers behind them. Sony, Nikon, and Canon have undoubtedly sold the story of the full-frame dream, however, they also have the capability and capacity to build out a system to support this — something Olympus has never quite been able to do.

The question for camera manufacturers is, does the future actually lie in the direction of the smartphone? Olympus (and Panasonic) have always been forthcoming in introducing computational features into their cameras and have extensive experience in working with, and manipulating imagery from, small sensors.

As smartphone sensors get bigger and processing becomes more complex, is there any scope to coalesce around an MFT future? In short, can the two companies capitalize on making smartphones camera-like and, conversely, can they also be leaders in making the camera more smartphone-like?